Aşağıda yayınladığımız yazılar, Özyeğin Üniversitesi, Financial Engineering and Risk Management (FERM) Yüksek Lisans Programında vermiş olduğum Financial Technologies dersinde öğrencilerimin bitirme ödevi olarak hazırladıkları çalışmalardan oluşmaktadır. Yazılar kendilerinden izin alınarak yayınlanmaktadır.

A missing part of the puzzle: Robo-Advisory

Hazırlayan: Sinem Ulusoy

Suppose that the financial markets would be a puzzle. The most important part of this puzzle is to make rational decision. We see that in general human behaviors are not rational because of cognitive, emotional and social biases. At this point, the robo-advisor constitute of missing part of a human who is in process of making decision. In this article I handle with the importance of robo advisory for investors.

This paper figure out firstly the concept of homoeconomicus and behavioral finance, then the evolution of the robo-advisor, the SWOT analyses of robo-advisory, the comparison of the robo-advisor with the human advisor and also a case from Turkey.

To be homoeconomicus or not

It’s known that humans are homoeconomicus in neo-classical economics. The concept of homoeconomicus based on theory of utility maximization (individuals maximize utility and firms maximize profits), the rationality and self-interest. Approach of homoeconomicus does not include any moral principles and the possibility of making mistake. Otherwise, human concept includes lots of mistakes which is generated result of some emotions or perceptions. However, associated with age of modern it’s realized that behaviors of human have affected everything. This behaviors are also not rational. As the behavioral economist Dan Ariely said: “We are more like Homer Simpson than Superman.” If the Superman was a reality, he would be a homoeconomicus.

The Markets and İrrational Human Behaviors

Associated with the global financial crises is noticed that human behaviors are not rational. Because many people especially in financial markets, move with herd behavior, optimism, emotions and all these behaviors result with irrationality. The irrational behaviors and decisions are called behavioral biases which are systematic errors in thinking. These biases are divided into three main categories: cognitive, emotional and social (Baker & Puttonen, 2017).The cognitive bias is type of mistake in thinking which is generated while a data is transformed into the information. Besides, according to Pompian (2006) the cognitive biases can handle with two major groups: belief perseverance biases and information processing biases. The emotional bias is taking action and decision-making rely on emotions. And finally, the social bias generates via external stimulus such as colleagues, culture even the internet. Especially in finance world, investors impress by others behaves. Even, typical social bias is herd behavior which is occurs generally due to the social pressure. We can also see these irrational patterns in Dan Ariely’s (Ariely, 2008) [1] questions, in particularly our decisions in daily life:

· Do you know why we so often promise ourselves to diet, only to have the thought vanish when the dessert cart rolls by?

· Do you know why we sometimes find ourselves excitedly buying things we don’t really need?

· Do you know why we still have a headache after taking a one-cent aspirin, but why that same headache vanishes when the aspirin costs 50 cents?

The money means that spending, saving or investing for people. Alright, in particular the concepts of saving and investing are much difficult in making decision process. Each of phases of making decision process include lots of uncertainties and biases. Especially when the market plummets, many inexperienced investors also tend to the irrational attitude (Baker & Puttonen, 2017). Therefore to better making a decision people need to the financial advisor who has more experience and knowledge. On the other hand, what if the financial advisor also would insufficient as to better making decision?

Evolution of The Robo-Advisory

The cutting-edge high technology offers to investors unconventional investment tools which is called robo-advisor. Robo advisor is an online software which advice rely on the user’s responses to a questionnaire filled out online (Fein , 2015). The first robo-advisor was created in 2008 and until 2010 development of the first robo-advisor continued. Bank of America developed a hybrid guided investing model in 2010. Into between 2013 and 2017 its adoption to technology was accelerated by human financial advisors. And finally, in 2017 Betterment which is an independent robo advisor is announced that it will adopt a hybrid model. The questionnaire which determine robo advisor’s advice includes knowledge about an individual’s who wants to investing risk tolerance and investment preference. The typical robo advisor questionnaire includes typical questions which identify the investors profile (Fein , 2015):

• Are you saving (i) for retirement, (ii) to build an emergency fund, or (iii) to maintain my standard of living?

• Do you understand stocks, bonds and ETFs (i) a lot, (ii) somewhat, or (iii) not at all?

• When you hear “risk” related to your finances, do you (i) become worried, (ii) remain indifferent, or (iii) see opportunity?

• Have you ever lost 20% or more of your investments in one year?

• If you ever were to lose 20% or more of your investments in one year, would you (i) sell everything, (ii) do nothing, or (iii) buy more?

• When it comes to making important financial decisions, do you (i) avoid them, or (ii) make them?

• How much fluctuation are you confident your investment will encounter in the next year — (i) a lot, or (ii) not much?

• How long do you expect to keep your money invested?

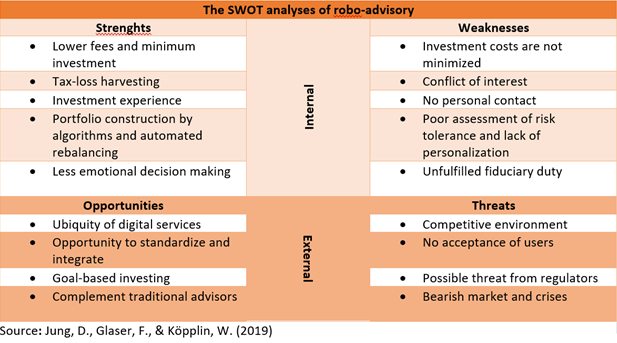

The SWOT Analyses of Robo-Advisory

In addition, the robo-advisory concept has a SWOT (Strenghts-Weaknesses-Opportunities- Threats), just like everything else.

The Robo Advisor versus Human Advisor

· The most significant feature that separates the robo advisor from human advisor is cost. The robo advisors have less expensive advisory fees in particularly in terms of less labor-intensive. Thus associated with this feature the robo advisors become more accessible for investors.

· The robo advisors are available at any time and location.

· The robo advisors are less likely to have conflicts of interest (Fisch, Laboure, & Turner, 2017)

On the other hand, the robo-advisors have been criticized that the questions in the robo-advisor questionnaire remain incapable to definition of an investor profile. Besides, when the market volatility soars a human advisor may be more understand that investor who is panic or individual’s investment needs.

A Case From Turkey

In 2017, the robo advisory which is quantitative and algorithmic model was launched by AKInvestment. With this robo advisory was aimed to obtain asset allocation. Thus, investor able to enhance their investment decision and also to increase saver’s profits. For instance, according to Akinvestment bulletin, The Robo Advisor tool presents valuation scores to nine EM markets under our scope, based on quantitative analyses and econometric models that rely on historical regression, real exchange rate (REER) comparisons and equity valuations. Thanks to the robo advisor tool investor comprehend signs of EM equities.

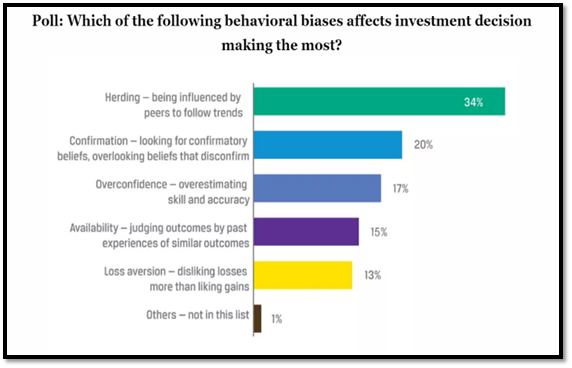

Source: (Kunte, 2016)

When we looked at this chart we see that the process of investment decision making is no rational. In particular, in uncertainty investors tend to follow herd and also some other behavior anomalies follow such as confirmation, overconfidence, availability, loss aversion. They make mistakes, show behavioral biases, and fall victim to investment traps because they lack of knowledge, experience, or self-discipline to make better choices. Especially the Subprime Mortgage Crisis tell us that investors have animal spirit which led to make errors and deficiency in rational decisions. So, investors are neither fully homo-economicus nor emotional. Indeed, as homo sapiens they have vague emotions (Turan & Latifi, 2013)

As a result, where the human behave irrational more is needed to robo advisor which less emotional decision making and based on algorithms. On the other hand, in terms of the companies robo advisory is less labor-intensive. Once upon a time while neo economists believed that concept of the human has homoeconomicus, nowadays behavioral economists believe that humans are not rational. As a investor make your choice: the robo advisor or human advisor?

This paper was prepared as a class work for Financial Technology course given by Prof. Selim YAZICI at Ozyegin University, Graduate School of Business, Financial Engineering and Risk Management Program.

References

Ariely, D. (2008). Predictably irrational. New York: An Imprint of Harper Collins Publisher.

Baker, H. K., & Puttonen, V. (2017). ınvestment Traps Exposed: Navigating Investor Mistakes and Behavioral Biases. Emerald Publishing Limited.

Baker, H. K., & Puttonen, V. (2017). Investment Traps Exposed: Navigating Investor Mistakes and Behavioral Biases. USA: Emerald Publishing Limited.

Fein , M. L. (2015). Robo-Advisors: A Clooser Look. 2.

Fisch, J. E., Laboure, M., & Turner, J. A. (2017). The Economics of Complex Decision Making: The Emergence of the Robo Adviser. 13–21.

Jung, D., Glaser, F., & Köpplin, W. (2019). Robo-Advisory-Opportunities and Risks for the Future of Financial Advsiory. ResearchGate, 11.

Kunte, S. (2016). Enterprising Investor. https://blogs.cfainstitute.org/:https://blogs.cfainstitute.org/investor/2015/08/06/the-herding-mentality-behavioral-finance-and-investor-biases/

Otto, P. E. (2010). Cognitive Finance, Behavioral Strategies of Spending, Saving and Investing. New York: Nova Science Publishers, Inc. .

Pompian, M. M. (2006). Behavioral Finance and Wealth Management: How to Build Optimal Portfolios That Account for Investor Biases. John Wiley & Sons, Inc.

Turan, G., & Latifi, P. (2013). Are Investors More Home Sapiens Rather Than Homo Economicus: A Behaviorist Approach to Financial Crisis. International Journal of Economics and Finance Studies, 176.

[1] Dan Arely is the Alfred P. Sloan Professor of Behavioral Economics at MIT.